Your Christmas Wish List: Fed Week

Your Christmas Wish List: Fed Week

Key Takeaways from this weeks events

Check out our - Best Articles | Twitter

theSTATreport^ is home of the “Your Christmas Wish List” series.

In this article:

Key Takeaways from this week’s speeches and interviews from the Fed Governor’s and Treas. Sec. Yellen

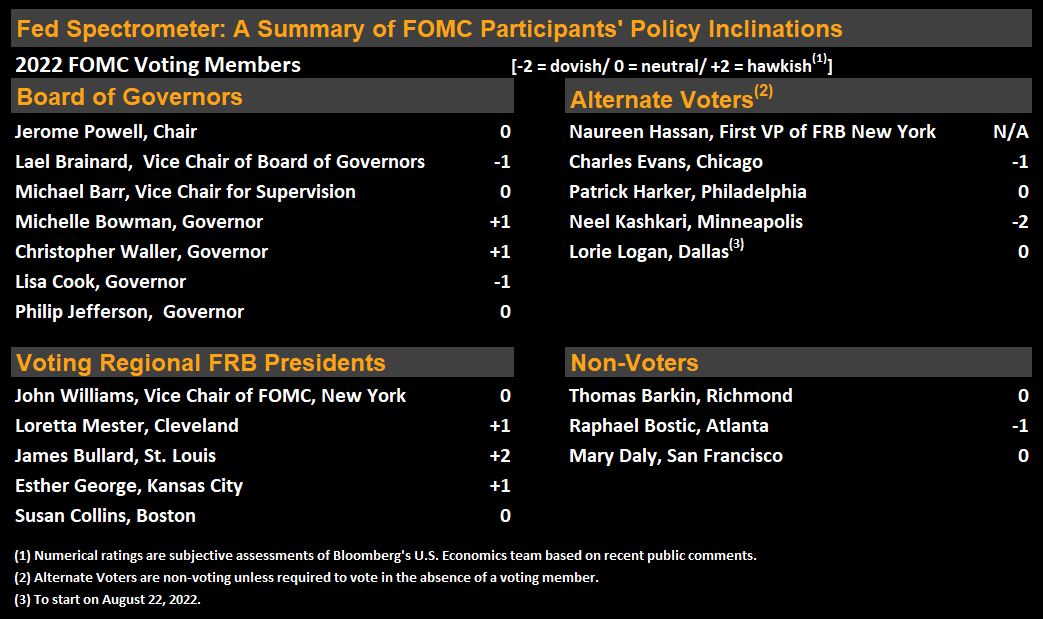

Charts

Short term real rates are negative as the short term rate is lower than expected inflation which makes current monetary policy still accommodative. So positive real rates means the short term rate is higher than expected inflation, which will make monetary policy restrictive. Estimate is 0.5%, or 50 bps, the policy rate needs to be at above inflation in order to be restrictive.

8/29 Fed Vice Chair Brainard comments in in remarks to FedNow workshop

Launch of Fed Now payment service likely May-July 2023

8/30 Richmond Fed Barkin speaks at event

Recession is risk in getting inflation under control

Seeing some slowing in interest-rate sensitive sectors

Fed will do what it takes to return inflation to 2%

will need positive real rates to control inflation

interest rates will need to be restrictive

8/30 Atlanta Fed’s Bostic comments in essay on banks website

Could dial back 75 bps hikes if prices clearly cooling

policy needs to be restrictive

8/30 NY Fed’s Williams at WSJ event

Focused on getting inflation back down to 2%

Restrict Fed policy needed through next year

Feds needs somewhat restrictive policy, not there yet

Decision on Sept. rate move hinges on data totality

8/30 Richmond Fed Barkin on Yahoo Finance

Won’t prejudge size of next rate hike, depends on data

Must move real rates to positive territory across curve

focused on getting rates to restrictive territory

There is a lag in impact from monetary policy

Inflation coming down through three ways 1) falling demand 2) healing supply chain challenges 3) commodities falling

8/31 Cleveland Fed Mester at Dayton Chamber of Commerce

Sees unemployment above 4% by year end

Does not anticipate Fed cutting rates next year

Hikes lead to below trend growth in nominal output for this year and next and higher unemployment rate

Can’t be precise yet on Fed’s terminal interest rate

Have to curb inflation even if that means a recession

Wage increases not keeping up with inflation and current wages are not consistent with our 2% goal

need wage growth to moderate to 3.25-3.5% for price stability

expects more progress with inflation moving down over the next two years but will require further action by the Fed to make that so

Will calibrate hikes based on economic outlook and monetary policy goals

Real rates need to move in positive territory and remain there for some time

Need several months in MoM declines in inflation to confirm inflation has peaked

8/31 Treasury Secretary Yellen

Substantial progress made on G-7 Russia Oil-Price Cap

Without a price cap, we face the threat of a global energy price spike if the majority of Russian energy production gets shut in

JP Morgan estimated oil at $380 in worst case scenario if Russia cut 5 mbd. $190 if Russia cut 3 mbd.

9/1 Atlanta Fed’s Bostic speaks to Business School students

Fed may have to sell MBS from balance sheet in future

Balance sheet to be increasingly MBS concentrated

Fed has got to get the economy to slow down

That is it for the week!

H=Hawk D=Dove

Payroll data moves Treasury market most

Sell 2Y/Buy 10Y flattens until hikes stop

Next week

If you found something of value within this article, please like and/or share it. Subscribe, if you are not subscribed. If you have a comment or question, please leave a comment or ask your question in the comments. This allows others to benefit from the interaction.

Charts, news, and/or data sourced from Bloomberg Professional unless otherwise noted.

TERMS OF USE

thestatreport.substack.com (“Site”) is a website owned and operated by Substack. By accessing this Site, any page thereof, or any social media account, you are indicating your consent and you agree to be bound by the Terms of Use and Disclaimer. The Terms of Use and Disclaimer may be amended from time to time.

DISCLAIMER

theSTATreport, its affiliates, respective owners, representatives, members, directors, officers, managers, agents, trustee’s, clients, friends, family, or employees (collectively, the “STAT Parties”) presents this communication and content for your informational purposes only. This material is for illustration and discussion purposes only and are not intended to be, nor should they be construed as, financial, legal, tax, or investment advice and does not constitute as an opinion, or recommendation, or advice, or offer, or solicitation by the STAT Parties.

Certain information has been provided by and/or is based on third party sources and although such information is believed to be reliable, STAT Parties makes no representation with respect to the accuracy, completeness, adequacy, or timeliness of such information. This information is being presented “as is” without warranty, express or implied, of any kind whatsoever. This information may be subject to change without notice. Everything is subject to revision by STAT Parties and STAT Parties is under no obligation to update, amend, modify, or supplement this publication, in whole or in part, or any of the information contained herein, under any circumstance.

Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Past Performance is not indicative of future results. Any prices or levels shown are either historical or purely indicative. Any projections, market outlooks, or estimates herein may be forward looking statements and are inherently unreliable. They may be based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Other events that were not taken into account may occur and may significantly affect the returns, performance, or outcome of everything mentioned herein. The information provided herein is based on matters as they exist as of the date of preparation and not as of any future date.

STAT Parties may from time to time enter into securities transactions, including, but not limited to, involving buying, selling short, hedging, in securities covered in this and other publications before or after a publication is issued. To the extent any of the STAT Parties have such positions, there is no guarantee that STAT Parties will maintain such positions. Any statement in this publication regarding performance is not indicative of, and does not guarantee future results, or that anticipated results, may be realized.

The recipient of this must make his/her/its own independent decisions regarding any legal, tax, securities, investment products, or other financial products mentioned herein. Seek independent professional consultation in the form of legal, investment, tax, and fiscal advice before making any investment, legal, tax, or financial decision. The information and opinions provided herein should not be taken as specific advice on the merits of any decision. The STAT Parties does not accept any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, form any use of the information contained herein.

Unauthorized reproduction of this newsletter or its contents by photocopy, facsimile or any other means is illegal and punishable by law.

Always perform your own due diligence.