Your Christmas Wish List: Fed Watch

Your Christmas Wish List: Fed Watch

Key Takeaways with Insights from recent events

Check out our - Best Articles | Twitter

theSTATreport^ is home of the “Your Christmas Wish List” series.

In this article:

Key Takeaways from recent speeches and interviews from Fed Governor’s, Summers, and Dudley

Insightful visuals relevant to recent Fed Speak

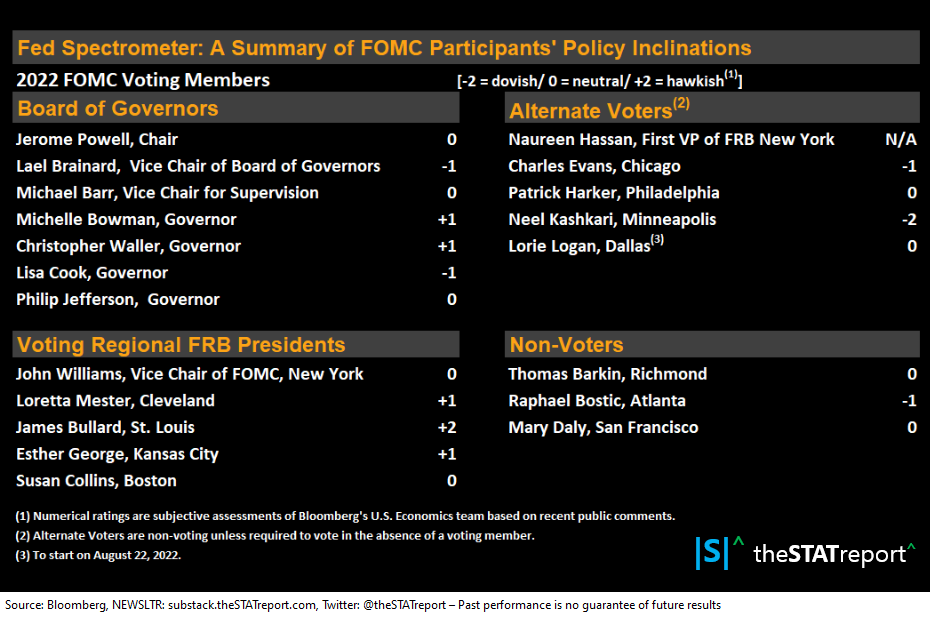

45 Key Stats the FOMC are watching. Compare recent values vs values at last FOMC meeting date

Blackout

Calendar of upcoming Fed related events

Informative Fed Watch research with charts and tables

Key Takeaway Highlights

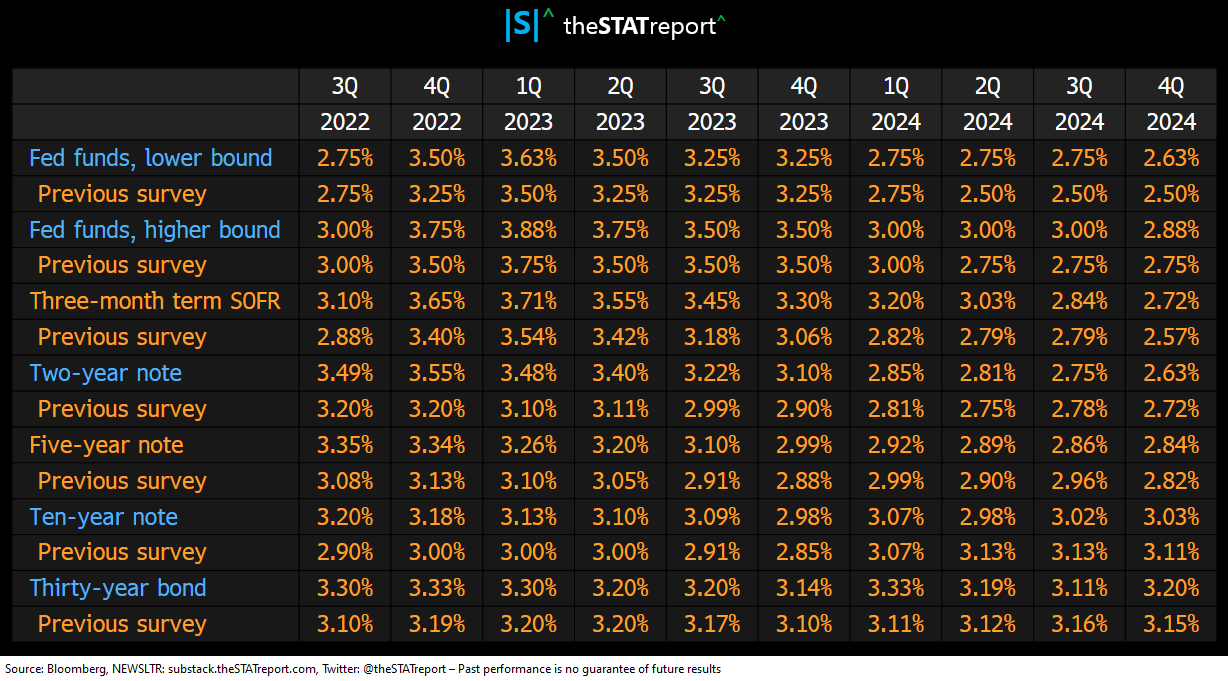

Rates could be well above 4% if prices don’t cool

Markets underpricing higher for longer rates

Fed must defend inflation expectations anchor

Good CPI report shouldn’t affect Sept. decision

Lots of wage pressure

Labor market key thing to watch

9/2 Larry Summers on Bloomberg’s Wall Street Week

Will be surprised if the Fed reaches their 2% inflation target without an unemployment rate that approaches or exceeds 6%

An increase in higher participation with the same unemployment rate means more people are working and earning and spending and that in turn will raise the demand for labor

9/6 Barkin interview by the FT

Bias in general towards moving more quickly

Rates must stay high until inflation eases

Real rates need to be above zero

9/7 Mester at MNI webcast

Backs Fed discussing MBS sales in future

Carefully watching gauges of inflation expectations

Doesn’t expect cuts in 2023

Backs Fed hiking rates above 4% by ‘23

Not convinced that inflation has peaked

Focus is path of rates, not size of hike at next meeting

9/7 Collins speaks in podcast

Inflation simply to high

Returning inflation to 2% is really job one

Premature to specify 9/21/22 policy decision

9/7 Brainard at event in New York

Uncertainty on policy lag creates overtightening risk

Takes time for full effect of tightening to be felt

Fed must defend inflation expectations anchor

Need several months of data to confirm slower inflation

Fed in it for as long as it takes to curb inflation

Lower retail margins to ease price pressure

Fight inflation for as long as it takes

Very focused on housing sector

Need for clear regulatory guardrails for crypto

Banks need to be intermediaries in a future US CBDC

9/7 Barr Speaks on Financial System Fairness and Safety in Washington

Committed to working to bring down inflation

Wants Congress to act on crypto Stablecoins

Fed’s role in dealing with climate change narrow

Focus on climate issues to be risk based

9/7 Fed’s Beige Book https://www.federalreserve.gov/monetarypolicy/beigebook202209.htm

High prices and a tight labor market weighed on US economic prospects

The outlook for future economic growth remained generally weak, with contacts noting expectations for further softening of demand over the next six to twelve months

Residential real estate weakened amid a drop in home sales in all districts

Price levels “remained highly elevated,” but nine districts reported some degree of moderation in their rate of increase

High prices and a tight labor market weighed on US economic prospects over the next year

9/8 Powell speaks at Monetary Policy Conference at Cato

History cautions against prematurely loosening policy. Fed will act forthrightly until Inflation job is done.

Very important that inflation expectations are anchored

Fed’s job is to ensure inflation expectations are anchored

Framework meant to anchor inflation expectations at 2%

Labor market demand remains very strong

Hope to receive period of growth below trend

Below trend growth will give better labor market balance

Money supply/Inflation relationship has been unstable

Monetary aggregates don’t play key role in policy

Don’t see dual mandate goals as being in conflict

Don’t see a case for Fed to move to a single mandate

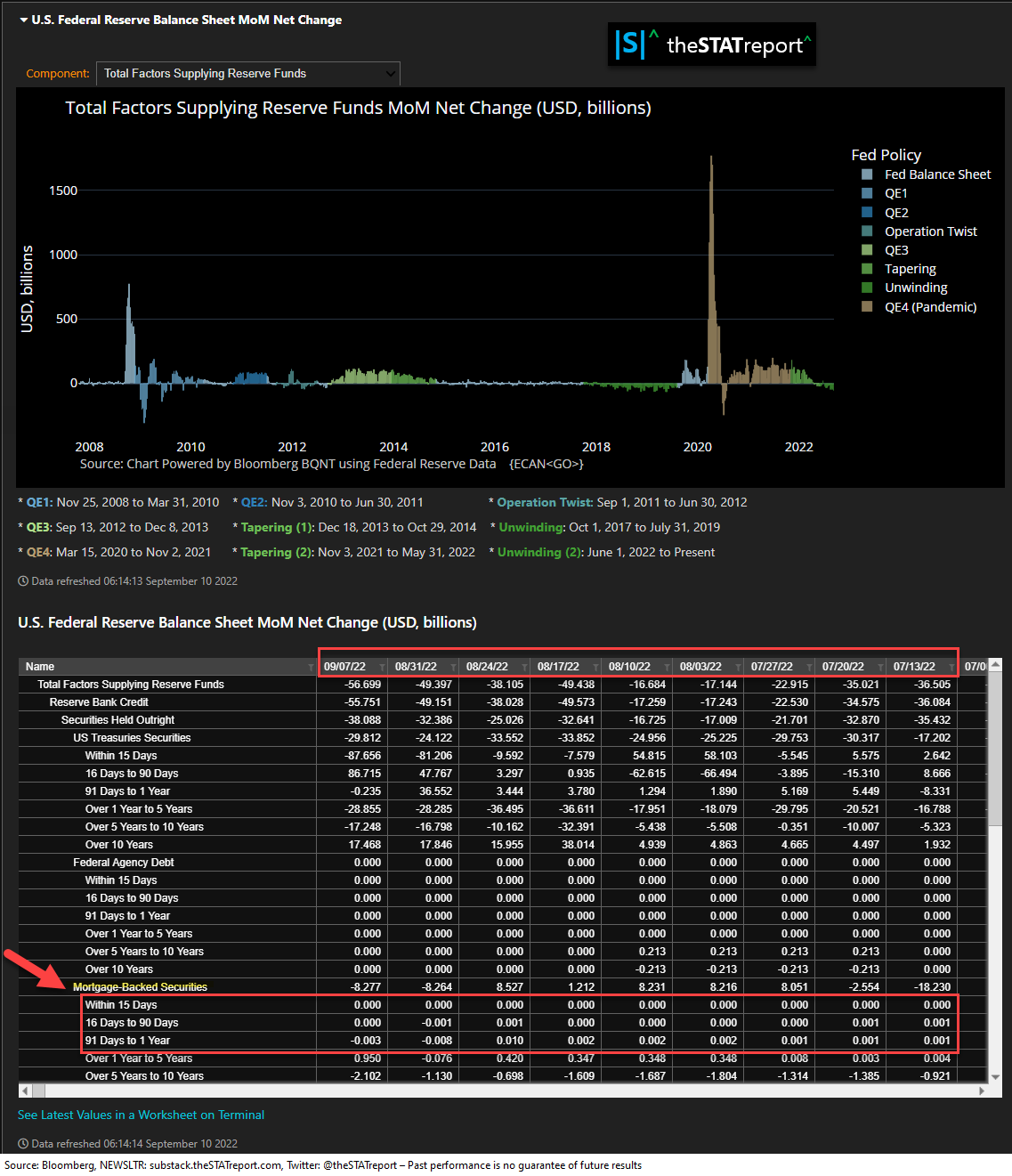

Prepared to adjust Balance Sheet runoff as economy needs

Crypto don’t appear to offer public interest as payment

Stablecoins can play a role in our financial system

Federal fiscal policy not on sustainable path. US needs to get back to sustainable fiscal path soon.

The neutral policy rate estimates are much less than inflation of 6.3% (Core inflation) as measured by the Fed’s preferred gauge. Consumers expect 4.8% inflation over the next year and 2.9% over five to 10 years, according to the University of Michigan’s survey.

UMich Inflation expectations

9/8 Evans speaks at DuPage forum

Possible that the number of vacancies can decline without serious increases in unemployment

Worry about inflation expectations getting out of hand

If the public begins to question our commitment to getting inflation back down then it could broaden out

Job one is to get inflation back to our 2% objective in some reasonable period of time

9/9 Bill Dudley in Bloomberg Interview

Key thing to watch is status of US Labor market

Labor market much to tight to be consistent with 2% inflation

Premature to say collective policy tightening overdone

Fed to have tighter policy for longer than most expect

Fed’s MBS worth less than Fed purchased them for. MBS underwater.

Thinks Fed won’t exacerbate MBS losses by selling mortgages and booking the losses

Fed’s return on assets will be less than the cost of their liabilities as Fed raises rates

9/9 Waller speaks at event in Vienna

If inflation slows, rates may peak under 4%

Rate peak could be well above 4% if prices don’t cool

Hike until compelling evidence prices cooling

Favors raising rates until at least early next year

Will watch to see if Fed QT impacting longer term rates

Fed Balance sheet shrinking may already be priced in

9/9 George with PIIE

Passthrough lag calls for steady, not fast, policy move

Fed can’t reverse supply shocks spurring prices

Fed must determine policy course through observation

Balance sheet trimming may involve asset sales

Supports getting back to Treasuries based balance sheet

Focused on path of rates, not individual meetings

Fed has some room to run and bring interest rates up

9/9 Bullard in Bloomberg interview

Leans more strongly to 75bp hike in Sept.

Good CPI report shouldn’t affect Sept. Fed call

Markets underpricing higher for longer rates

Rates after catch up will be more flexible

Labor market tight, lots of wage pressure

45 Key Stats the FOMC are likely watching. Compare recent values vs values at last FOMC meeting date.

Blackout Calendar. Starts 9/10/22 through the 22nd.

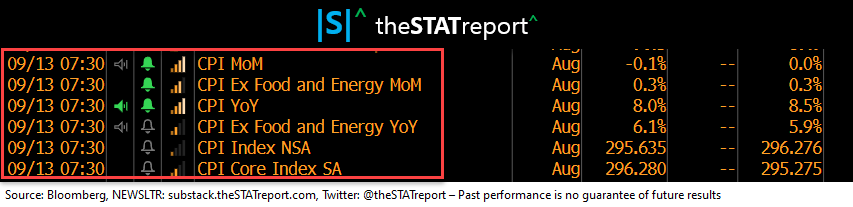

CPI report on 9/13 during Blackout

Calendar of Upcoming Fed Related Events

Informative Fed Watch Research

MoM CPI

ISM Gauge Shows the Economy Can Take Aggressive Hikes

If potential GDP growth indeed has slowed, the Fed will have to engineer an even larger decline in the economy than anticipated to generate the “sustained period” of below-trend growth Powell said would be needed.

More hikes despite plunging global GDP. Potentially lasting implications for asset prices and deflation.

M2. What stops a normal dump in commodities?

Mean reversion of risks. Crude Oil and T-Bond futures

YoY PPI stretch to match 1974.

US Federal Funds Target Interest Rate History

A stabilization in liquidity has likely been a major factor in risk assets recovery since June, the Treasury (TGA) component has masked the tightening coming directly from the Fed and the private sector.

If you found something of value within this article, please like and/or share it. Subscribe, if you are not subscribed. If you have a comment or question, please leave a comment or ask your question in the comments. This allows others to benefit from the interaction.

TERMS OF USE

thestatreport.substack.com (“Site”) is a website owned and operated by Substack. By accessing this Site, any page thereof, or any social media account, you are indicating your consent and you agree to be bound by the Terms of Use and Disclaimer. The Terms of Use and Disclaimer may be amended from time to time.

DISCLAIMER

theSTATreport, its affiliates, respective owners, representatives, members, directors, officers, managers, agents, trustee’s, clients, friends, family, or employees (collectively, the “STAT Parties”) presents this communication and content for your informational purposes only. This material is for illustration and discussion purposes only and are not intended to be, nor should they be construed as, financial, legal, tax, or investment advice and does not constitute as an opinion, or recommendation, or advice, or offer, or solicitation by the STAT Parties.

Certain information has been provided by and/or is based on third party sources and although such information is believed to be reliable, STAT Parties makes no representation with respect to the accuracy, completeness, adequacy, or timeliness of such information. This information is being presented “as is” without warranty, express or implied, of any kind whatsoever. This information may be subject to change without notice. Everything is subject to revision by STAT Parties and STAT Parties is under no obligation to update, amend, modify, or supplement this publication, in whole or in part, or any of the information contained herein, under any circumstance.

Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Past Performance is not indicative of future results. Any prices or levels shown are either historical or purely indicative. Any projections, market outlooks, or estimates herein may be forward looking statements and are inherently unreliable. They may be based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Other events that were not taken into account may occur and may significantly affect the returns, performance, or outcome of everything mentioned herein. The information provided herein is based on matters as they exist as of the date of preparation and not as of any future date.

STAT Parties may from time to time enter into securities transactions, including, but not limited to, involving buying, selling short, hedging, in securities covered in this and other publications before or after a publication is issued. To the extent any of the STAT Parties have such positions, there is no guarantee that STAT Parties will maintain such positions. Any statement in this publication regarding performance is not indicative of, and does not guarantee future results, or that anticipated results, may be realized.

The recipient of this must make his/her/its own independent decisions regarding any legal, tax, securities, investment products, or other financial products mentioned herein. Seek independent professional consultation in the form of legal, investment, tax, and fiscal advice before making any investment, legal, tax, or financial decision. The information and opinions provided herein should not be taken as specific advice on the merits of any decision. The STAT Parties does not accept any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of the information contained herein.

Unauthorized reproduction of this newsletter or its contents by photocopy, facsimile or any other means is illegal and punishable by law.

Always perform your own due diligence.