In Focus: CPI

Check out our - Best Articles | Twitter

theSTATreport^ is home of the “In Focus” series. A data-driven, in-depth, evidence-based series about the US Fed, FOMC, and US Economy.

In this article:

Highlights on CPI

Scenario Analysis for Shelter

Think Ahead — Reflective thoughts to keep in mind regarding the Fed.

Are the forward market pricing and Fed communication about the forward rate move expectations the same? They both can’t be right if they are on different paths. Think about cause and effect. What are the current conditions that support current thinking - and why - for the FOMC and market participants? What are some potential likely paths this may play out?

What characteristics does the labor market need to have for the Fed to have 2% inflation?

How does the Fed think about their dual mandate? What key stats are they watching, what are they looking for in those stats, and over what time frame?

With the Fed’s dual mandate, in the future when unemployment starts to rise and if inflation is still to high, how will they approach that scenario?

Fed in Blackout.

Wall Street (1987) - Anacott Steel

If the Fed will do what they have been saying, the market still has some adjustments to make within it’s pricing and today it seems pricing is getting more closely realigned with past Fed communications.

Strong CPI.

Fed’s larger focus of the two is Core CPI (Ex Food and Energy).

More Evidence of

wages are feeding into prices

inflation is broadening out, including services

Energy fell again (5% vs 4.6% last report)

Little Evidence of

Firms offering steep discounts to liquidate excess inventories

No Evidence of

Rents peaking

Labor accounts for +50% of output. With labor rising at approx. 10% in 1H ‘22, firms should be motivated to boost prices. As discussed before, consumers getting higher wages gives them increased spending power thereby helping maintain higher demand.

MoM CPI % change, weighted highest to lowest.

Sticky inflation1 has a tendency to stick around.

Shelter MoM%

Shelter YoY%

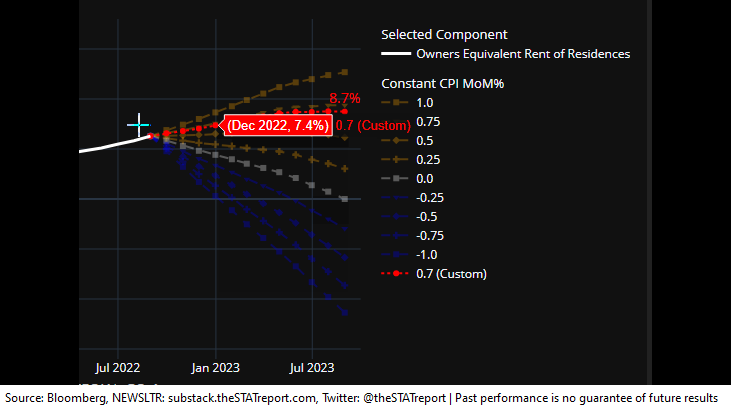

Projection Assumption Scenario

Shelter makes up 32% of the index. Using the August MoM shelter #, lets see how this # may influence the forward YoY CPI #.

Rent of Shelter, Owners Equivalent Rent, and Owners Equivalent Rent of Primary Residences.

Shelter probably will peak sometime within 1H ‘23. Larry Summers thinks we’ll have upward pressure in the CPI report for shelter for 6 - 9 more months.

Core CPI YoY will likely increase in coming months.

All the Fed members have made it clear they are looking for several months of broad based evidence that inflation is coming down.

Which circle’s back to this articles subtitle.

If you found something of value within this article, please like and/or share it. Subscribe, if you are not subscribed. If you have a comment or question, please leave a comment or ask your question in the comments. This allows others to benefit from the interaction.

TERMS OF USE

thestatreport.substack.com (“Site”) is a website owned and operated by Substack. By accessing this Site, any page thereof, or any social media account, you are indicating your consent and you agree to be bound by the Terms of Use and Disclaimer. The Terms of Use and Disclaimer may be amended from time to time.

DISCLAIMER

theSTATreport, its affiliates, respective owners, representatives, members, directors, officers, managers, agents, trustee’s, clients, friends, family, or employees (collectively, the “STAT Parties”) presents this communication and content for your informational purposes only. This material is for illustration and discussion purposes only and are not intended to be, nor should they be construed as, financial, legal, tax, or investment advice and does not constitute as an opinion, or recommendation, or advice, or offer, or solicitation by the STAT Parties.

Certain information has been provided by and/or is based on third party sources and although such information is believed to be reliable, STAT Parties makes no representation with respect to the accuracy, completeness, adequacy, or timeliness of such information. This information is being presented “as is” without warranty, express or implied, of any kind whatsoever. This information may be subject to change without notice. Everything is subject to revision by STAT Parties and STAT Parties is under no obligation to update, amend, modify, or supplement this publication, in whole or in part, or any of the information contained herein, under any circumstance.

Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Past Performance is not indicative of future results. Any prices or levels shown are either historical or purely indicative. Any projections, market outlooks, or estimates herein may be forward looking statements and are inherently unreliable. They may be based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Other events that were not taken into account may occur and may significantly affect the returns, performance, or outcome of everything mentioned herein. The information provided herein is based on matters as they exist as of the date of preparation and not as of any future date.

STAT Parties may from time to time enter into securities transactions, including, but not limited to, involving buying, selling short, hedging, in securities covered in this and other publications before or after a publication is issued. To the extent any of the STAT Parties have such positions, there is no guarantee that STAT Parties will maintain such positions. Any statement in this publication regarding performance is not indicative of, and does not guarantee future results, or that anticipated results, may be realized.

The recipient of this must make his/her/its own independent decisions regarding any legal, tax, securities, investment products, or other financial products mentioned herein. Seek independent professional consultation in the form of legal, investment, tax, and fiscal advice before making any investment, legal, tax, or financial decision. The information and opinions provided herein should not be taken as specific advice on the merits of any decision. The STAT Parties does not accept any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of the information contained herein.

Unauthorized reproduction of this newsletter or its contents by photocopy, facsimile or any other means is illegal and punishable by law.

Always perform your own due diligence.

Sticky Price Index consists of: Food Away from Home; Household Furnishings and Supplies; Infants and Toddlers Apparel; Medical Care Commodities; Alcoholic Beverages; Personal care products; Miscellaneous Personal Goods; Rent of Primary Residence; Owners Equivalent Rent of Primary Residence; Water, Sewer and Trash Collection Services; Medical Care Services; Motor Vehicle Maintenance and Repair; Motor Vehicle Insurance; Public Transportation; Recreation Services; Education and Communication Services